4 min read • about 2 months ago

Most retirement planning focuses on one goal:

Save enough money.

But once retirement arrives, the question changes.

It is no longer:

How much have I saved?

It becomes:

How much can I spend?

Unfortunately, many retirees never get a clear answer.

As a result, they often spend far less than they could comfortably afford.

Not because they lack money.

Because they lack confidence.

Many retirees fear running out of money more than they fear not enjoying retirement.

That fear is understandable.

Retirement may last 25 or 30 years.

Healthcare costs may rise.

Markets may decline.

Inflation may persist.

The result?

Many retirees choose to spend conservatively even when their plan could support more.

Portfolio:

$1.5 Million

Retirement Income Need:

$8,000/month

Actual Spending:

$5,500/month

In some cases, retirees spend thousands less per month than their plan could potentially support.

Many investors rely on simple rules such as:

The 4% Rule

While useful as a starting point, retirement spending is rarely one-size-fits-all.

Two households with identical portfolios may have very different outcomes because of:

That is why retirement spending should be personalized.

Instead of asking:

Can I afford this?

Ask:

How does this decision affect my retirement plan?

For example:

Current Spending:

$6,000/month

Potential Spending:

$6,800/month

Impact:

Success Rate:

94% → 92%

Ending Balance:

$620,000 → $480,000

For some retirees, spending an additional $800 per month may have very little impact on long-term retirement success.

Without testing scenarios, they may never know.

Most retirees don't know if they're spending too much or too little.

That's because there is rarely one correct answer.

Instead, there are multiple possible strategies.

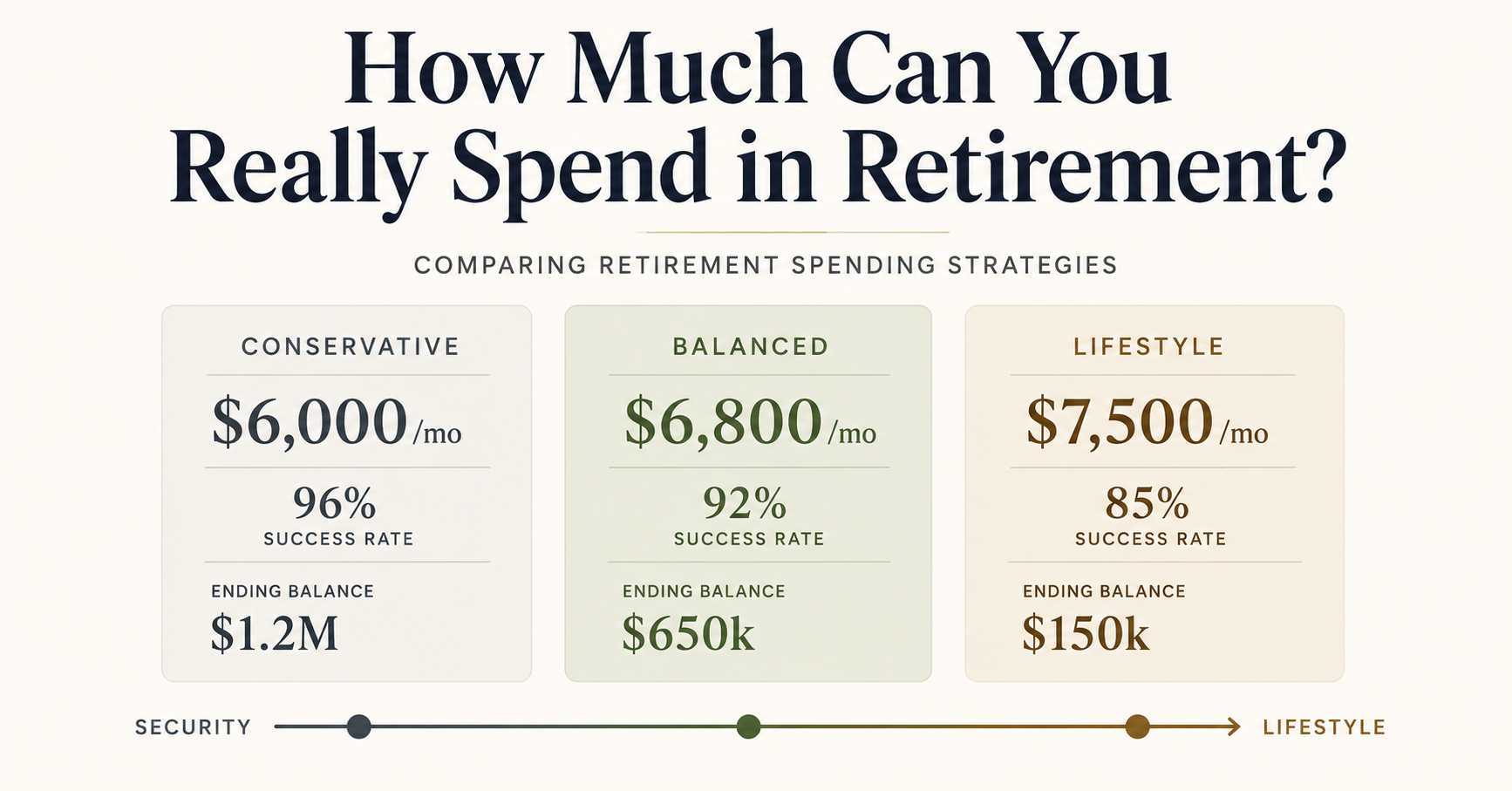

Monthly Spending:

$6,000

Success Rate:

96%

Ending Balance:

$1.2M

Monthly Spending:

$6,800

Success Rate:

92%

Ending Balance:

$650k

Monthly Spending:

$7,500

Success Rate:

85%

Ending Balance:

$150k

None of these strategies are automatically right or wrong.

The best choice depends on your goals.

Some retirees prioritize leaving a legacy.

Others prioritize maximizing retirement experiences while they are healthy enough to enjoy them.

The key is understanding the tradeoffs before making a decision.

Retirement spending is not about finding one perfect withdrawal amount.

It is about finding the strategy that best matches your priorities.

Some people want:

Each objective may lead to a different optimal strategy.

That is why retirement planning should focus on outcomes, not rules.

Imagine being able to compare:

Current Plan

vs

Spend More

vs

Spend Less

vs

Delay Social Security

vs

Work Part-Time

vs

Retire Earlier

Then seeing how each option affects:

That creates a much clearer picture than relying on a single projection.

Most retirement tools provide a single projection.

Nestly helps you explore alternatives.

Using Nestly Lab, you can generate and compare multiple retirement strategies side by side.

For example, you can test:

Nestly then evaluates each strategy across factors such as:

AI ranks the alternatives and highlights the tradeoffs so you can understand which strategy best aligns with your goals.

Because retirement planning isn't about finding a single answer.

It's about finding the strategy that fits the future you want to create.

One million dollars can last very different lengths of time depending on spending, Social Security, healthcare, and retirement age. Compare common scenarios and see what really drives retirement longevity.

Retiring before 65 can create a healthcare coverage gap before Medicare begins. Learn how to plan for ACA coverage, COBRA, spouse insurance, cash reserves, and healthcare bridge strategies.

Wondering how much net worth you need to retire? Learn why there is no single magic number and how spending, income sources, timing, and healthcare shape retirement readiness.