"How much should I contribute to my 401(k)?" is one of the most common questions in personal finance. The answer depends on your age, income, goals, and current financial situation.

This comprehensive guide will help you find your optimal contribution rate.

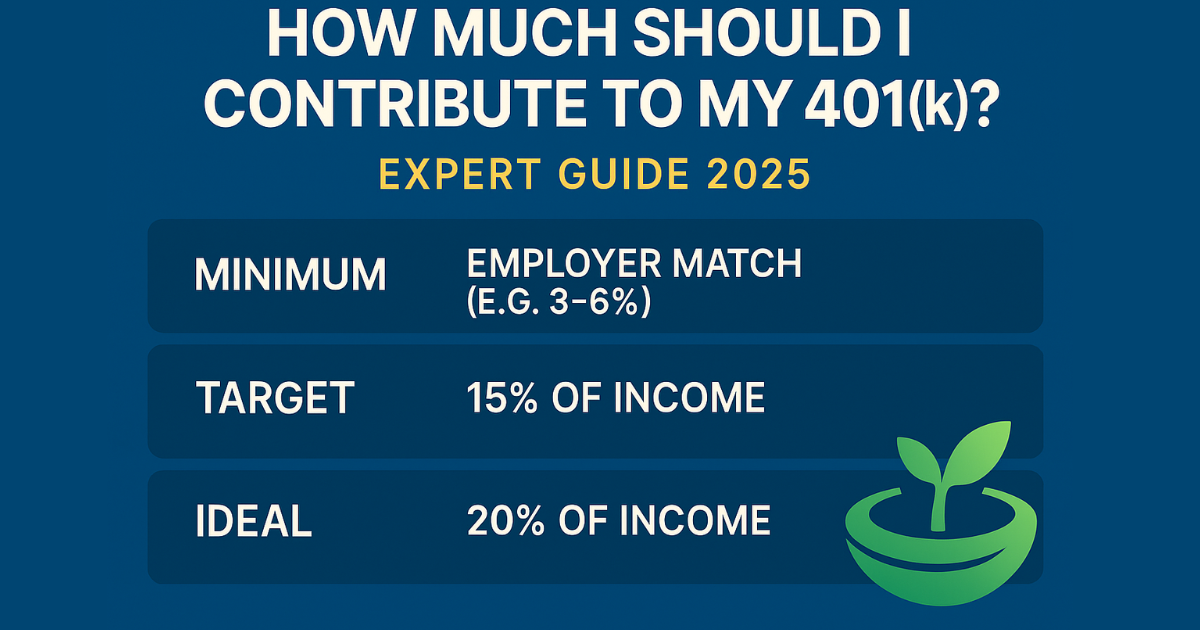

The Quick Answer (TL;DR)

Minimum: Contribute enough to get full employer match (usually 3-6%) Good: 10-15% of gross income including employer match Great: 15-20% of gross income Maximum: $23,500 in 2025 ($31,000 if 50+)

Now let's dive into the details.

1. Always Capture the Full Employer Match

This is free money you're leaving on the table if you don't take it.

Common Employer Match Formulas

50% match up to 6%: Contribute at least 6% to get 3% match

100% match up to 3%: Contribute at least 3% to get 3% match

Dollar-for-dollar up to 5%: Contribute at least 5% to get 5% match

Real Example

Your salary: $80,000

Employer offers: 50% match up to 6%

You contribute: 6% = $4,800

Employer adds: $2,400

Total savings: $7,200 (9% of salary)

Not taking the match is like declining a 50% raise on your contribution.

2. Contribution by Age (Rule of Thumb)

Here's a general guideline for total retirement savings rate (including employer match):

Age Range

Recommended Rate

Why

20s

10-15%

Time is your biggest asset - compound growth

30s

15-20%

Career growth, maximize compound interest

40s

20-25%

Catch-up time, peak earning years

50+

25-30%

Utilize catch-up contributions, final push

The "Start Young" Advantage

Starting at 25 vs 35:

Monthly contribution: $500

Annual return: 7%

Retirement age: 65

Start at 25: $1.2 million Start at 35: $566,000

That 10-year delay costs you $634,000 — more than doubling your result by starting early.

3. The 15% Total Savings Rule

Many financial advisors recommend saving 15% of gross income for retirement (including employer match).

Example Breakdown

Your salary: $70,000

Target savings: 15% = $10,500/year

Employer match: 4% = $2,800/year

Your contribution needed: 11% = $7,700/year

Why 15%?

Historical data suggests 15% sustained over 30+ years allows you to retire with similar lifestyle

Accounts for Social Security supplementing (but not relying on it)

Provides cushion for market downturns

4. Balancing 401(k) vs Other Goals

Contributing to 401(k) is crucial, but not the only financial priority.

Enter your current situation (age, salary, balance)

Set your retirement goals (age, lifestyle)

Test different contribution rates (10%, 15%, 20%)

See your projected outcome (Monte Carlo simulation)

Find your optimal number (balance goals vs current budget)

Quick Calculator Formula

Rough estimate for retirement readiness:

Target retirement savings = Current age × Current salary ÷ 2

Examples:

Age 30, Salary $60,000: Should have $30,000 saved

Age 40, Salary $80,000: Should have $40,000 saved

Age 50, Salary $100,000: Should have $50,000 saved

Behind? Increase contributions to catch up.

Action Steps: Start Today

Log into your 401(k) account — Check current contribution rate

Verify employer match — Make sure you're getting it all

Calculate 15% of salary — Set this as your target

Increase gradually — Up 1-2% now, 1% annually

Automate increases — Set it and forget it

Review annually — Adjust with raises/life changes

The Bottom Line

Minimum: Employer match (usually 3-6%) Target: 15% total savings (you + employer) Ideal: 20%+ if you can afford it Maximum: $23,500 ($31,000 if 50+)

Remember: The perfect contribution rate is the one you can sustain. It's better to contribute 10% consistently than to contribute 20% and have to stop.

Start where you are, use what you have, do what you can.

401(k) Contribution Limits for 2026: IRS Updates Explained

The IRS has officially released 401(k) and IRA contribution limits for 2026. Learn the new limits, catch-up rules, and how Nestly’s Contribution Co-Pilot helps you optimize savings.

NA

Nestly Advisor

3 min read

Read & Try

Retirement Planning

8 months ago

5 Smart Ways to Maximize Your Retirement Savings in 2026

Discover proven strategies to boost your retirement savings in 2026, including higher IRS contribution limits, employer match optimization, and smart planning with Nestly.

NT

Nestly Team

4 min read

Read & Try

Retirement Planning

about 2 months ago

The Social Security Mistake That Could Cost Married Couples Over $100,000

Many couples claim Social Security at the same age without realizing it may reduce lifetime benefits. Learn how coordinated claiming strategies can improve retirement income and long-term financial outcomes.