6 min read • about 12 hours ago

You are saving for retirement.

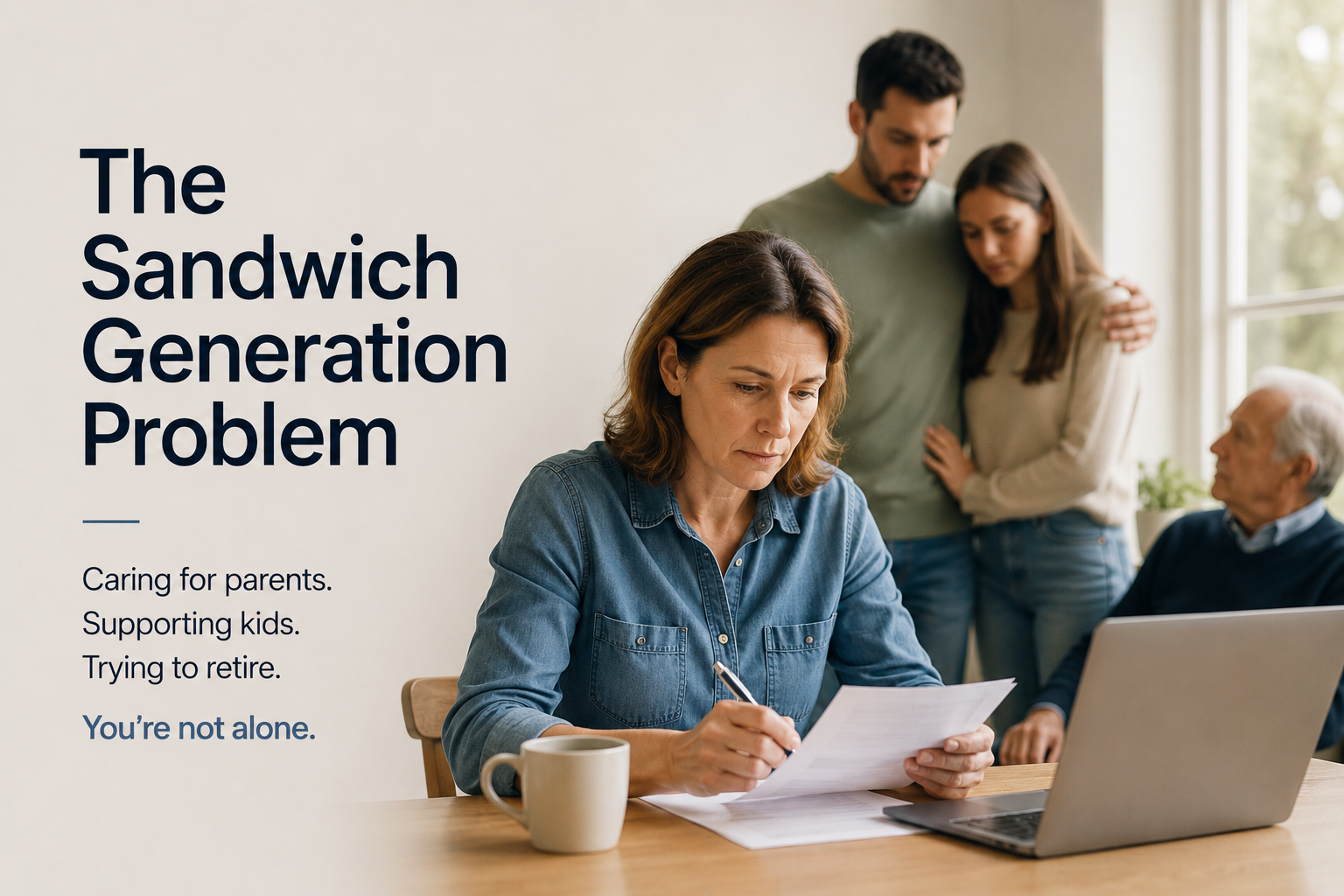

Your adult child needs help with rent.

Your aging parent needs medical, housing, or daily care support.

Your own retirement clock is still ticking.

That is the sandwich generation problem.

Many adults in their 40s, 50s, and early 60s are financially and emotionally supporting multiple generations at once.

The challenge is not whether you care about your family.

The challenge is figuring out how to help without putting your own retirement at risk.

The sandwich generation refers to people who are supporting both:

Support can take many forms.

It may include:

Some support is financial.

Some is emotional.

Some is time-based.

All of it can affect retirement planning.

Family support often starts small.

But small amounts can become large over time.

Parent Support:

$700/month

Adult Child Support:

$500/month

Total Monthly Support:

$1,200/month

Over 10 years:

$1,200/month x 12 months x 10 years

= $144,000

That $144,000 could affect:

This does not mean you should never help family.

It means the impact should be visible.

Sandwich generation planning is difficult because every choice protects something important.

| Priority | What It Protects | Potential Risk |

|---|---|---|

| Help Parents | Care, dignity, safety | Retirement savings may decline |

| Help Children | Stability, opportunity, support | Dependence may grow |

| Protect Retirement | Future independence | Emotional guilt or family tension |

There is rarely a perfect answer.

The goal is to find a balance that protects both your family and your future.

Family support becomes risky when it starts weakening your own financial foundation.

Warning signs include:

One of the biggest risks is open-ended support.

Without limits, temporary help can quietly become permanent.

Helping family does not have to mean writing unlimited checks.

A more sustainable approach is to create structure.

| Strategy | How It Helps |

|---|---|

| Set a monthly cap | Prevents open-ended support |

| Use one-time help | Easier to plan around |

| Share costs with siblings | Reduces pressure on one person |

| Pay bills directly | Keeps support targeted |

| Require a timeline | Prevents permanent dependency |

| Protect retirement first | Reduces future burden on children |

Boundaries are not a lack of generosity.

They are what make generosity sustainable.

Before committing to ongoing support, compare the retirement impact.

| Scenario | Monthly Family Support | Possible Retirement Impact |

|---|---|---|

| No Support | $0 | Maximum flexibility |

| Limited Support | $500 | Often manageable |

| Moderate Support | $1,200 | Meaningful tradeoff |

| Heavy Support | $2,500+ | Retirement may be delayed |

Even if you choose to help, knowing the tradeoff helps you make a more informed decision.

Money conversations can be uncomfortable.

But avoiding them usually makes the problem harder.

Helpful questions include:

These questions shift the conversation from emotion alone to planning.

Many parents and adult children understand this rule clearly:

You can borrow for college, housing, or emergencies. You cannot borrow for retirement.

That does not mean retirement should always come before every family need.

But it does mean your future independence deserves serious protection.

If helping today causes you to become financially dependent on your children later, the support may not be truly helping the family long term.

Instead of asking:

Can I help my family?

Ask:

Can I help my family without sacrificing my own future independence?

That question creates a healthier balance.

It allows room for generosity.

But it also protects the future version of yourself.

Family support decisions are retirement scenarios.

With Nestly Lab, you can compare:

AI then ranks each path based on retirement income, success probability, portfolio longevity, and flexibility.

Because the goal is not to stop helping family.

It is to help wisely while protecting your own future.

Wondering how much net worth you need to retire? Learn why there is no single magic number and how spending, income sources, timing, and healthcare shape retirement readiness.

Many parents want to support adult children, but financial help can affect retirement timing, portfolio longevity, and future independence. Learn how to evaluate the tradeoff.

Wondering if you're on track for retirement at age 50? Learn common retirement savings benchmarks, what counts as retirement savings, and how to evaluate your readiness.