5 min read • 8 months ago

Albert Einstein allegedly called compound interest “the eighth wonder of the world.” Whether or not he actually said it, the idea behind the quote is undeniably true.

Compound interest is one of the most powerful forces in personal finance—and one of the most misunderstood.

Compound interest means earning interest on your interest. Instead of your money growing in a straight line, it grows exponentially because every year’s gains become part of the base that earns future returns.

Time, not effort, does most of the work.

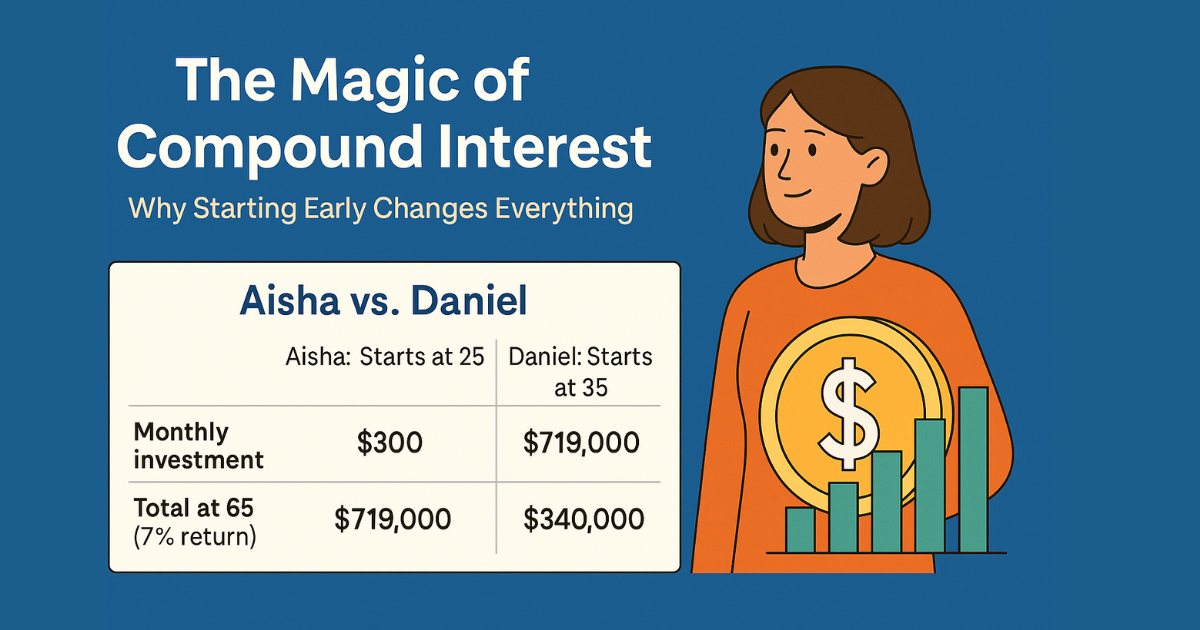

Let’s move away from abstract math and look at a realistic scenario.

Both graduate from college. Both land decent jobs. Both plan to retire at 65. Neither considers themselves a “finance person.”

The only difference?

When they start.

Total contributed: ~$144,000

Total contributed: ~$108,000

Aisha only invested $36,000 more, yet ends up with nearly $380,000 more at retirement.

This difference didn’t come from smarter investing or higher income—it came from time.

Many people believe they’ll “just save more later.” The math doesn’t support that.

Compound growth accelerates in later years, meaning:

By the time Aisha turns 45, her balance grows faster without increasing contributions—because compounding is doing the heavy lifting.

Want a quick mental model?

Years to double your money = 72 ÷ annual return

This means:

You can’t “catch up” to that without extreme savings later.

This is why people in their 40s and 50s often feel behind—even with higher incomes.

Compound interest becomes even more powerful inside tax-advantaged accounts.

Every matched dollar compounds just like your own.

The compound interest formula:

A = P × (1 + r)^t

You can’t control markets—but you can control:

Of the three, time is the most powerful.

You cannot replicate time with effort later.

Every interruption breaks the compounding engine.

Most people understand compound interest intellectually—but don’t feel its impact until it’s visualized.

That’s where tools like Nestly Advisor come in.

With Nestly, you can:

When people see their future balance jump by hundreds of thousands from small changes, behavior changes.

🚀 Start immediately — even small amounts compound

⏰ Time matters more than income

💰 Consistency beats intensity

📉 Interruptions are expensive

📈 Visualization drives action

Compound interest doesn’t care about intentions—it only responds to time and consistency.

The difference between starting at 25 and 35 isn’t a decade.

It’s financial freedom vs. financial stress.

The best day to start investing was 10 years ago.

The second best day is today.

If you want to see what compound interest can realistically do for your situation, Nestly’s calculator helps you model your future—not guess at it.

See estimated 401(k) balances by spending level, understand what changes the number, and compare retirement strategies with Nestly Lab.

Many people buy gold jewelry as an investment, but is it actually a good wealth-building strategy? Compare gold jewelry and investment gold to understand the real costs, risks, and long-term returns.

Juneteenth is a reminder that freedom and opportunity are deeply connected. Explore why access to financial education, investing, and retirement planning plays a critical role in building long-term financial freedom.