4 min read • 6 months ago

This article has a ready-to-run scenario — apply it to your own plan in one tap.

Many people assume that by their late 50s, retirement savings are largely “figured out.”

But recent data suggests otherwise.

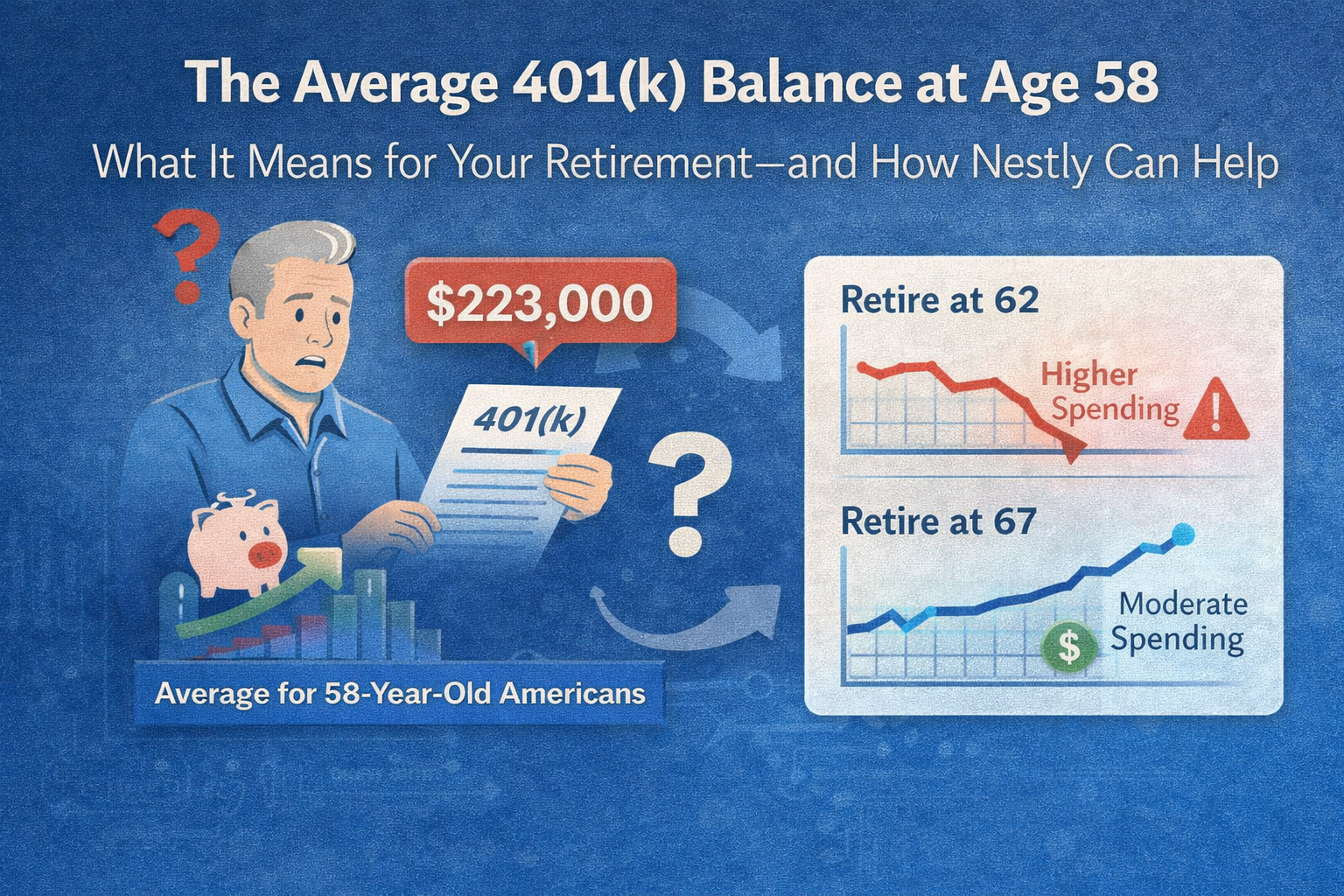

According to recent reporting, the average 401(k) balance for Americans around age 58 is significantly lower than most people expect—often falling short of what’s needed to sustain a comfortable retirement.

This isn’t a judgment. It’s a reality check.

And more importantly, it’s a moment of opportunity.

When you see an “average” retirement balance, it’s important to understand what that number does—and doesn’t—tell you.

In other words, the average balance doesn’t reflect what you personally need—only what’s common.

At age 58, many people are just 7–10 years away from retirement.

At that stage, savings must support:

A balance that looks “okay” on paper may still translate into:

The real question isn’t:

“How do I compare to the average?”

It’s:

“What does my current trajectory mean for my future income?”

Most retirement shortfalls aren’t caused by one big mistake—they’re caused by small, repeated decisions over decades.

Common reasons include:

By the time someone reaches their late 50s, the margin for error becomes smaller—but the opportunity to course-correct still exists.

Comparing yourself to the “average” can create false comfort—or unnecessary panic.

What actually matters is:

This is why retirement planning must shift from balance-focused to outcome-focused.

Nestly is designed to help you answer the questions averages can’t.

Instead of showing a single number, Nestly helps you:

For someone in their late 50s, this clarity is critical.

Imagine two 58-year-olds with the same 401(k) balance:

Their outcomes can be dramatically different.

Using Nestly, you can visualize:

This turns uncertainty into actionable decisions.

Even if you’re behind the “average,” you’re not out of options.

Key levers still available:

The most important step is understanding which lever matters most for you.

The average 401(k) balance at age 58 tells a story—but it’s not your story.

What matters isn’t how you compare to others.

It’s whether your plan aligns with:

With the right tools and clarity, even late-stage adjustments can meaningfully improve retirement outcomes.

The goal isn’t perfection. It’s preparation.

Related Reading

Want to see what your current savings really mean for your future?

Use Nestly to project your retirement scenarios and make informed decisions—before time runs out.

See how a 4% contribution increase helps close the gap to a stronger retirement balance.

Wondering if you're on track for retirement at age 50? Learn common retirement savings benchmarks, what counts as retirement savings, and how to evaluate your readiness.

Discover how retirement savings vary across generations, what benchmark ranges look like by age, and how to determine whether you're on track for retirement.

Compare investing more for retirement with paying off your mortgage early. See how interest rates, employer matches, taxes, retirement timing, and risk can change the answer.