5 min read • 6 months ago

This article has a ready-to-run scenario — apply it to your own plan in one tap.

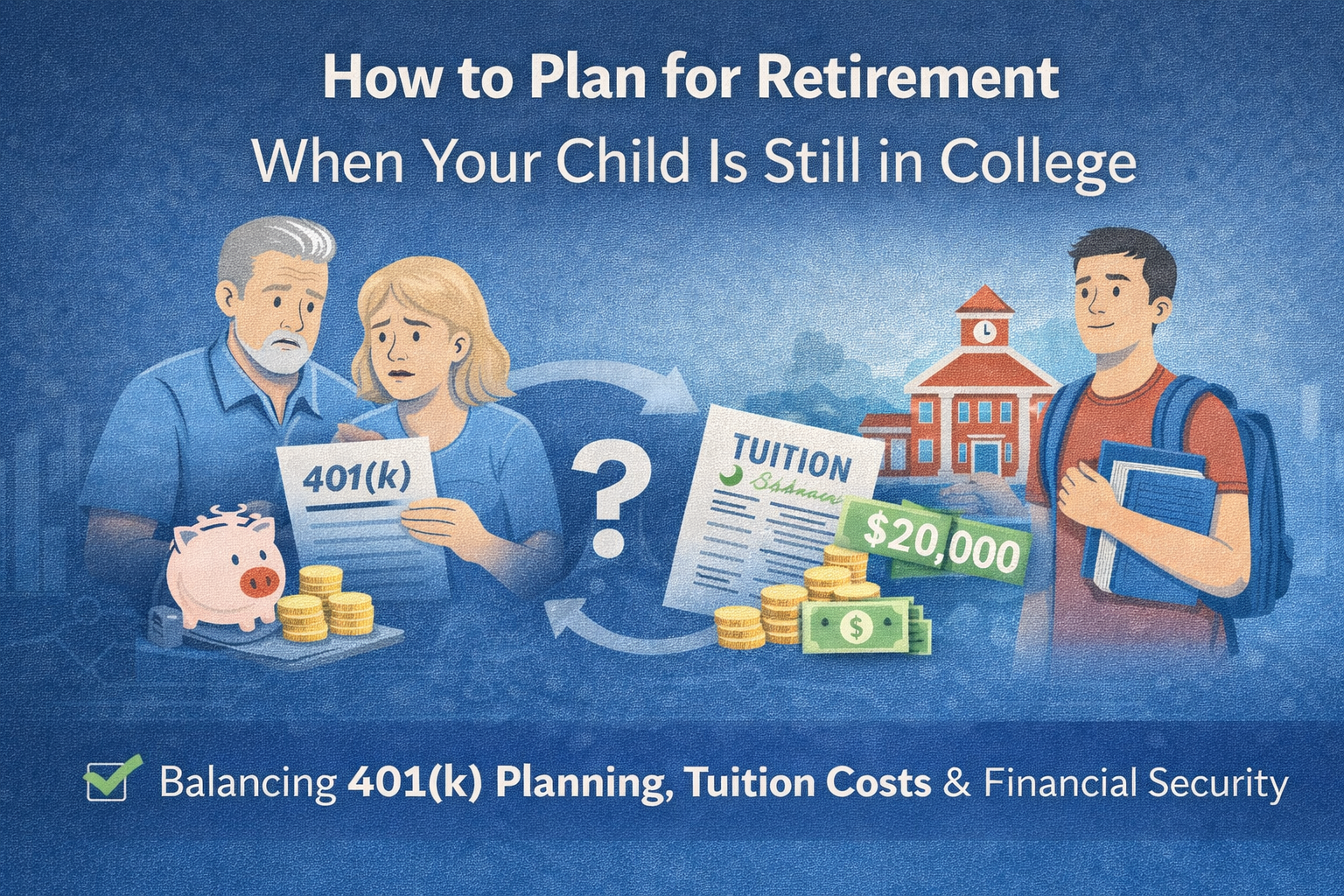

For many families, the traditional timeline doesn’t apply anymore.

Parents are retiring later.

Children are going to college longer.

And increasingly, those two phases overlap.

If you’re approaching retirement—or already retired—while still helping pay for a child’s college education, you’re not alone. But this overlap introduces real financial tradeoffs that require careful planning.

The key is not choosing retirement vs. college — it’s balancing both without putting your long-term security at risk.

Several trends are converging:

As a result, it’s increasingly common for parents to be:

This can feel uncomfortable to hear — but it’s essential.

There are loans for college.

There are no loans for retirement.

Sacrificing retirement security to fully fund college can lead to:

Helping your child is admirable. But protecting your financial independence is part of helping them too.

When retirement and college overlap, expenses peak:

At the same time:

This is why cash flow planning matters more than account balances during this phase.

It’s easy to overextend out of guilt or pressure. Start with numbers:

Clarity reduces stress — for both you and your child.

Withdrawing from a 401(k) early (or excessively) can:

If withdrawals are necessary, plan them intentionally and understand their long-term impact.

Instead of fully covering tuition, consider:

This shares responsibility while preserving retirement security.

Small adjustments can make a big difference:

Even modest income during early retirement can significantly reduce portfolio strain.

Retirement assets are often treated differently than income in financial aid formulas.

Understanding how:

affect aid eligibility can help you avoid unintended consequences.

When college overlaps with retirement:

This is where static rules of thumb fall short.

Nestly helps families visualize tradeoffs instead of guessing.

With Nestly, you can:

Instead of asking “Can I afford this?”

You can ask “What happens if I do?”

That clarity empowers better decisions — without regret.

Think of this phase not as a failure of planning, but as a complex transition.

You’re:

There’s no perfect solution — only informed ones.

If your child is still in college when you retire:

Protect your retirement first.

Support your child thoughtfully.

Plan with clarity, not guilt.

The goal isn’t to fund everything — it’s to ensure everyone moves forward securely.

Related Reading

Want to see how college expenses impact your retirement plan?

Use Nestly to model real-life scenarios and make confident, informed choices.

See the tradeoff of trimming your contribution rate to fund tuition instead of delaying retirement.

Buying a car around retirement is common—but it can quietly strain your retirement plan. Learn how to budget, time, and fund a car purchase without hurting long-term income.

As America celebrates 250 years of independence, it's a reminder that financial independence is built through planning, flexibility, and thoughtful decisions. Here's your own Declaration of Financial Independence.

Many couples claim Social Security at the same age without realizing it may reduce lifetime benefits. Learn how coordinated claiming strategies can improve retirement income and long-term financial outcomes.